Barley Market Report: Strong Demand Pulls Down Canadian Barley Ending Stocks in 2025/26

This barley market report was provided by Leftfield Commodity Research.

Estimated reading time: 4 minutes

Key Takeaways

- 2025/26 Canadian barley supplies are the largest in five years, but strong demand has steadily eroded the expected large carryout

- Livestock feed use is tracking at ~5.65 mln tonnes — a five-year high — as competitive barley prices boosted feeding relative to last year

- Exports of 3.01 mln tonnes through week 42 are the strongest since 2020/21; the final total may exceed 3.50 mln tonnes, with China the top buyer and Saudi Arabia returning after nearly a decade

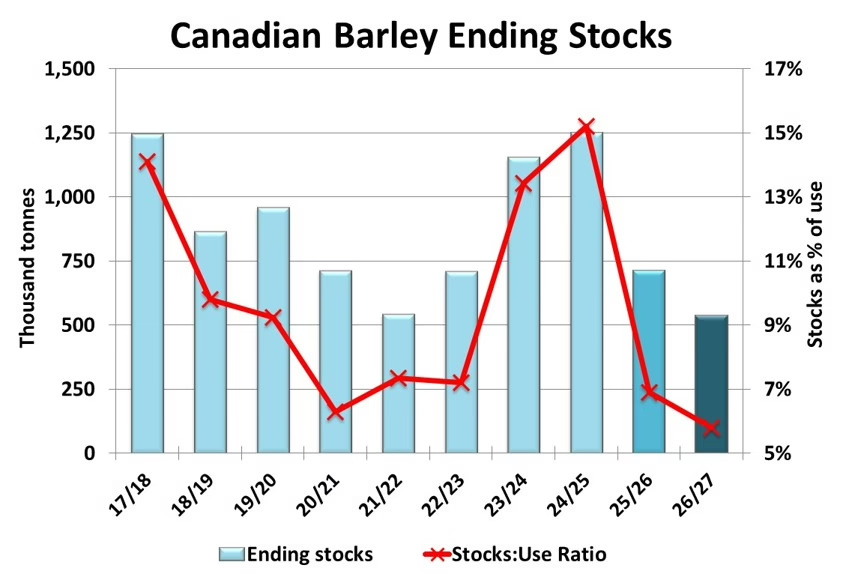

- Total usage could reach ~10.32 mln tonnes in 2025/26 — up 26% from 8.22 mln tonnes in 2024/25 — pulling down ending stocks and driving prices higher despite large starting supplies

- The 2026/27 balance sheet is set to tighten further; higher seeded area may not fully offset a return to normal yields from last year’s record

- The price outlook hinges on external factors: US corn competition for feed demand, competitor crop conditions, and the scale of Chinese barley purchases

Canadian barley supplies in 2025/26 are the largest in five years, led by big production of 9.73 mln tonnes (according to StatsCan, and it’s possible the crop was even larger) and a higher old-crop carryin. This set early expectations for a sizeable carryout at the end of the season. However, that assumption has been consistently walked lower as demand exceeds initial estimates at the start of the year.

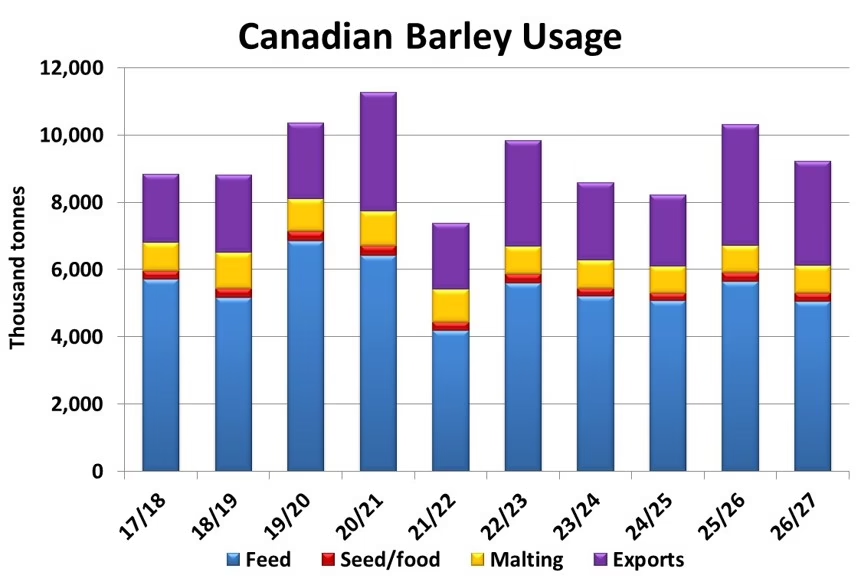

Canadian Barley Feed Demand Reaches a Five-Year High

Livestock feeding is the largest source of barley demand. It is hard to measure precisely, and supply and disposition tables often use the Feed/Waste/Dockage category as a bit of a ‘catch all’ to make the rest of the numbers balance. For this reason, official feeding estimates need to be taken with a grain of salt. Even so, StatsCan data is a reasonable indicator of the general trend. StatsCan’s March 31st stocks figure reported feed use at 600,000 tonnes higher than last year and above the 5-year average. This could point to 2025/26 feeding of around 5.65 mln tonnes, the most since 2020/21.

Canadian Barley Exports Surge to Multi-Year Highs

Exports have also been strong this season. CGC data shows barley exports at 3.01 mln tonnes as of week 42, the most since 2020/21, helped by Canadian barley being very competitive in global markets. Volumes typically drop off into the end of the season, but it’s possible the final total may exceed 3.50 mln tonnes. China has been the primary destination, but movement to Japan is also way up this year, while Canada shipped barley to Saudi Arabia for the first time in nearly a decade.

Record Usage Tightens 2025/26 Ending Stocks

Big feeding and exports could put total usage this season of around 10.32 mln tonnes, far above the 8.22 mln tonnes in 2024/25 and the highest since 2020/21. The result is a drop in ending stocks in 2025/26 as strong demand has drawn down inventories, and the reason prices have been increasing despite the large starting supply.

Canadian Barley Outlook for 2026/27: Prices and Key Risks

The early setup is for the Canadian barley balance sheet to tighten even further in 2026/27. StatsCan’s initial estimate for 2026 barley area came in 6.44 mln acres, up from the 6.14 mln in 2025. It’s likely final plantings are even higher, perhaps close to 7.00 mln acres or more. Even so, it’s possible production ends up being smaller if yields decline from last year’s record to more normal levels. Lower supplies will force a drop in consumption, as stocks simply won’t allow for a repeat of the feed and export disappearance experienced this year.

All else equal, the outlook for even tighter ending stocks in 2026/27 is supportive for prices. But whether or note that is the case may depend as much on external factors as Canadian barley supplies. Feed usage can be backfilled with other prairie cereal production and US corn imports, making the US corn outlook important for prairie barley values.

Export movement is also uncertain next season. Barley crops in other key exporters shape demand for Canadian supplies. Very early indications suggest production may be lower across most key exporters, which keeps Canada as an important supplier, but most of the growing season is still ahead. On the demand side, China has represented between one-third and half of global barley trade in recent years. Their purchases are influenced by domestic feed grain production and how competitive barley prices are relative to other substitutes. This leaves a wide range of potential scenarios for the Canadian barley outlook in 2026/27, despite a relatively tight starting point.

Find more barley market reports here:

- Barley Market Report: Tighter Global Supplies Set to Support Canadian Barley Prices in 2026/27

- Barley Market Report: USDA and StatsCan Update 2026 Barley Acreage Estimates

- Barley Market Report: Strong Demand Pulls Down Canadian Barley Ending Stocks in 2025/26

- Barley Market Report: Early Guesses for 2026 Canadian Barley Production

- Barley Market Report: North American Barley Acreage Projections for 2026