Barley Market Report: North American Barley Acreage Projections for 2026

This barley market report was provided by Leftfield Commodity Research.

Key Takeaways

- Canadian barley outlook is likely understated in StatsCan’s initial acreage estimate, with seeded area potentially closer to 7.0 million acres as stronger prices emerged after the survey period.

- Production may still decline in 2026 despite higher acreage if yields revert from last year’s record levels toward a longer‑term average.

- US barley acres remain near historical lows, limiting growth in North American supply and reinforcing Canada’s role in meeting demand.

- Acreage decisions remain fluid as farmers respond to volatile crop prices, rising fertilizer costs, and dry conditions across parts of Western Canada.

- Corn market dynamics will be critical for barley price direction, with lower US corn acreage increasing weather sensitivity through the growing season.

- June 30 acreage reports from StatsCan and USDA will be a key checkpoint for confirming final planted area and refining supply expectations.

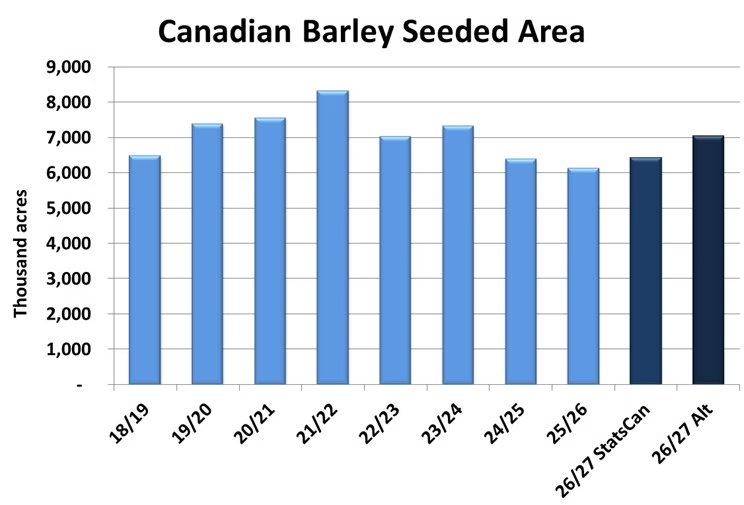

Canadian Barley Acreage Expected to Increase in 2026

StatsCan’s initial estimate for 2026 Canadian barley seeded area came in at 6.4 mln acres, 5% higher than the 6.1 mln planted last season, and compared to the 5-year average of 7.1 mln acres. It’s quite likely barley plantings on the prairies will be higher than initially shown. The farmer survey took place from mid-December to mid-January, and won’t have captured the firming in both old-crop and new-crop barley prices that has taken place since then.

It’s possible Canadian barley plantings end up closer to 7.0 mln acres. While this would be a sizeable 14% increase from 2025, it’s important to keep in mind that last year’s area was the smallest since 2017. In this sense, even if barley area ends up well above the initial StatsCan figure, it could still be on the lower end of what was common from 2019 to 2023, which included a recent high of 8.3 mln acres in 2021.

Yield Normalization Could Limit Production Gains

Despite the increase in plantings, a return to average yields from last year’s record could see Canadian production decline in 2026. For example, using a 5-year olympic average yield of 65.0 bu/acre (which takes the average after removing the largest and smallest figures) translates into 9.0 mln tonnes of production, down from 9.7 mln in 2025.

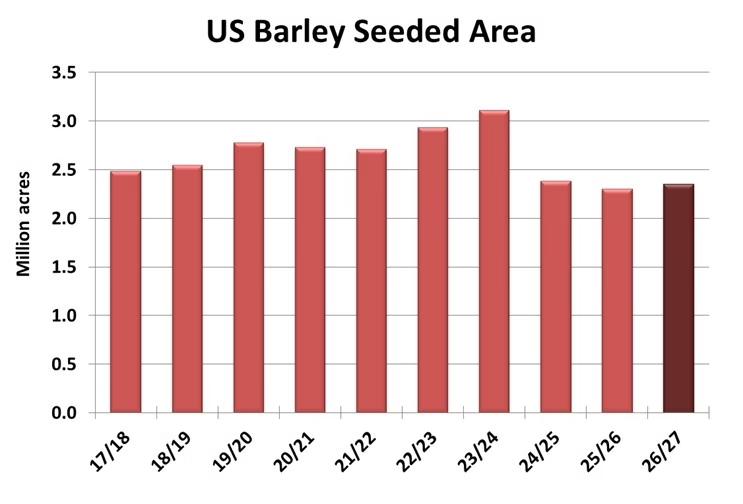

US Barley Acres Remain Structurally Low

USDA’s estimate for US barley area came in at 2.4 mln acres, up a modest 53,000 acres from last year, and remaining near a historical low. This compares to a 5-year average of closer to 2.7 mln acres. More so than in Canada, US barley acres are getting squeezed by other crops, likely keeping them at a structurally low level going forward.

Assuming an average yield, US barley production would be around 3.0 mln tonnes, which is close to the previous two seasons. Combined North American production might be roughly 12.0 mln tonnes, near the 5-year average.

Acreage Volatility and Late‑Season Switching Risks

This season has the potential for more last-minute acreage switching in Canada than most other years. Prices have been volatile, and returns in many instances didn’t look particularly attractive though much of the winter, which could result in farmers pushing rotations for certain crops at the expense of others in a search for profitability. The spike in fertilizer prices may also shift some area. And parts of western Canada are on the dry side going into spring, which may affect decisions. Barley acres will likely benefit overall, but the situation is fluid. This will leave some acreage uncertainty until the next round of government reports. Both StatsCan and USDA will release updated acreage figures on June 30th, which will be a better reflection of what farmers actually put in the ground.

Corn Market Signals Remain Critical for Barley Pricing

Finally, Canadian barley prices are heavily influenced by the US corn market. USDA’s initial survey-based estimate put 2026 corn plantings at 95.3 mln acres, which is down from last year’s huge 98.8 mln, although above pre-report expectations. A return to a trendline yield may result in production of around 16 bln bushels, down from the 2025 record of 17 bln, but still the second largest crop ever. Early indications suggest the 2026/27 corn balance sheet will be comfortable, but the combination of lower seeded area and strong demand will keep the market very sensitive to weather all season.

Find more barley market reports here:

- Barley Market Report: North American Barley Acreage Projections for 2026

- Barley Market Report: Largest December 31st Canadian Barley Stocks Since 2019

- Barley Market Report: USDA Increases US Corn Production Estimates

- Barley Market Report: A Big 2025 Canadian Barley Crop Will Result in Larger Ending Stocks

- Barley Market Report: Could Barley Demand Surprise to the Upside in 2025/26?